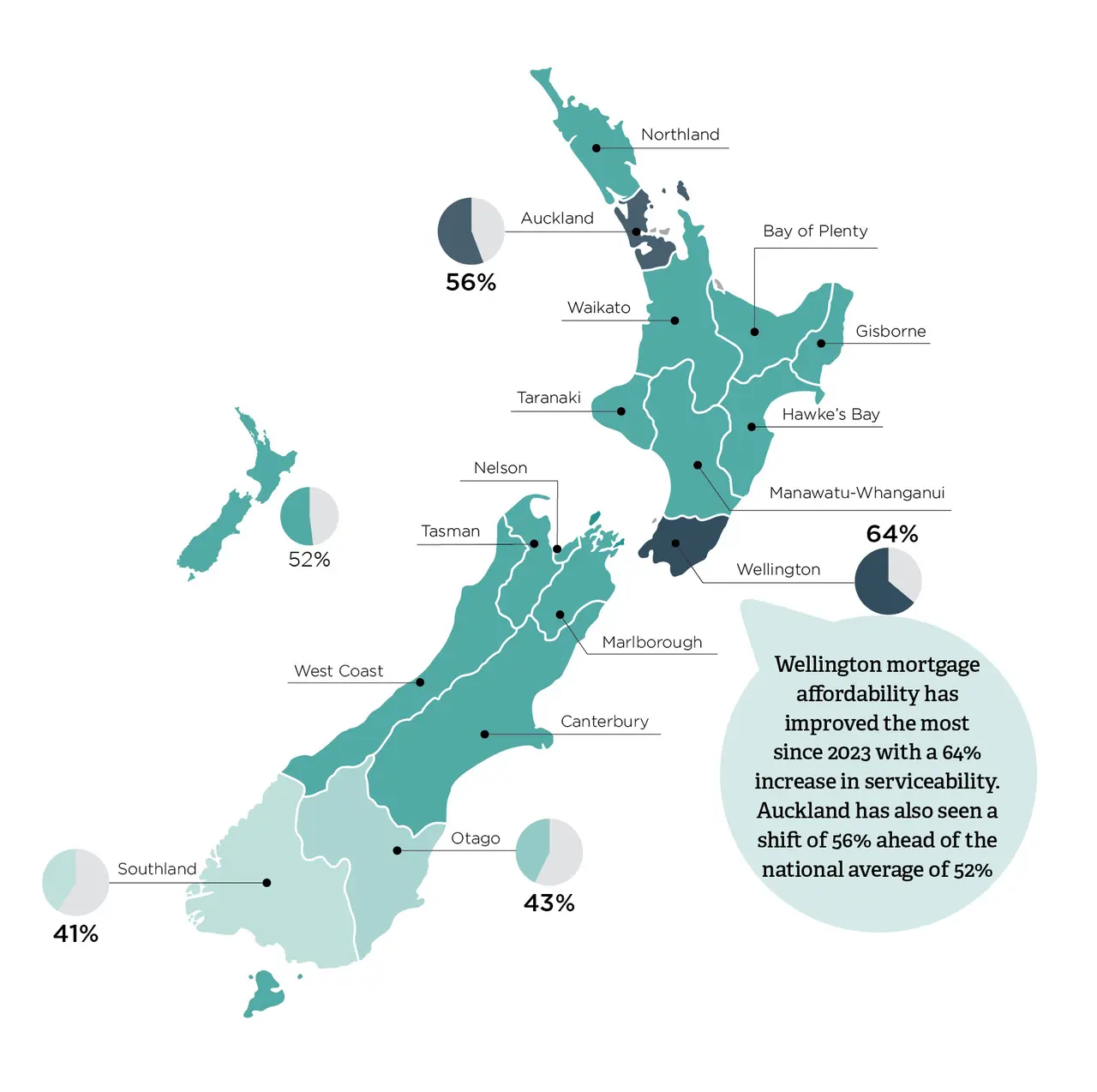

Auckland follows closely with a 56% lift, as falling mortgage rates and stable house prices ease pressure on buyers.

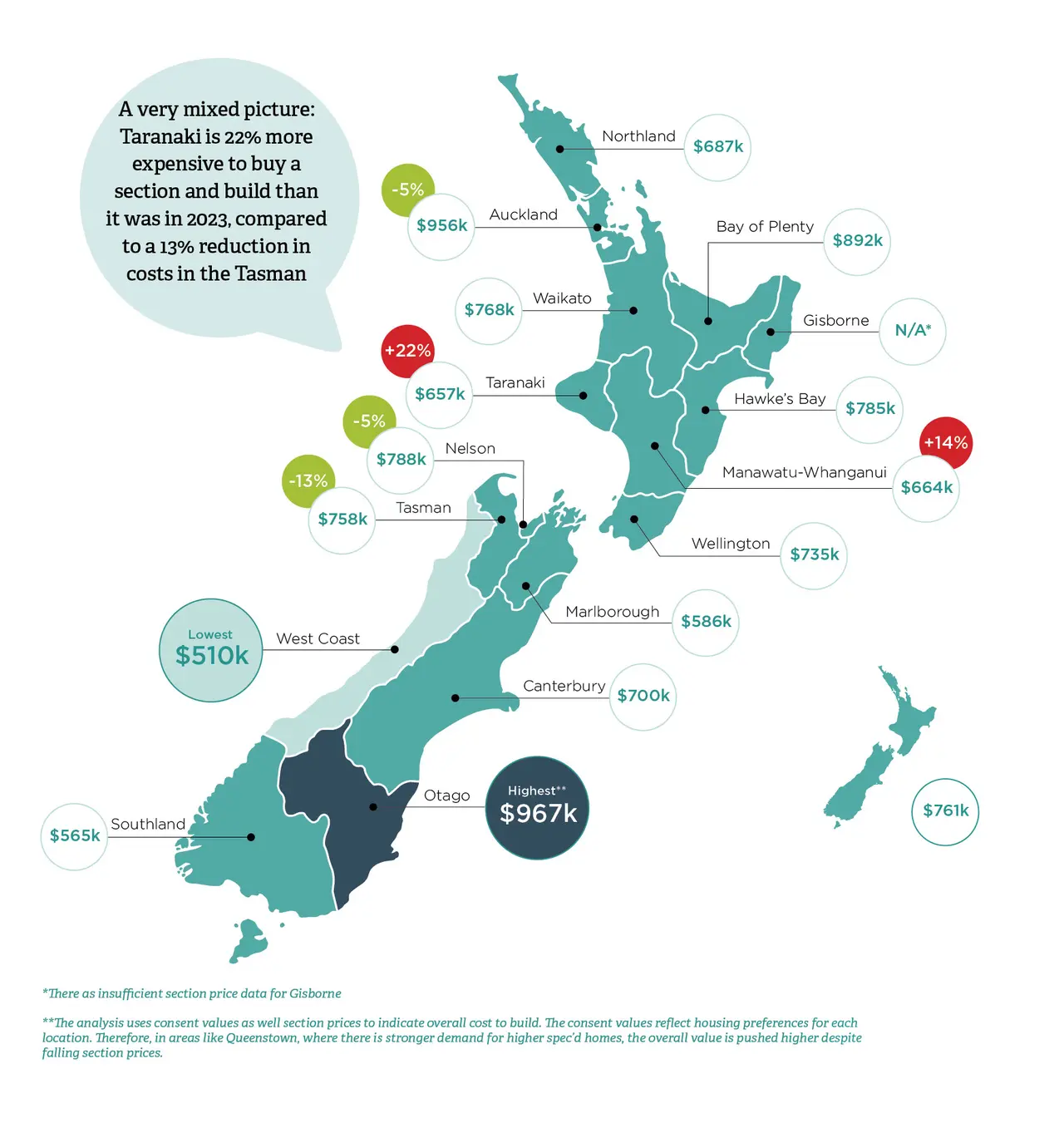

Section prices in urban centres have dropped 16% over the past year, and construction costs have stabilised. Together, these shifts are creating real opportunities for first-home buyers to purchase or build, marking a significant turnaround with conditions moving in a more favourable direction.

These insights come from the BRANZ Build Insights data tool which combines multiple trusted datasets in one place, updating them as new information comes out. Seeing the indicators side by side gives a fuller picture of medium to long-term housing and construction trends. The tool provides a comprehensive view of affordability, mortgage rates, construction activity, consents process, price pressures and regional variations - helping industry and New Zealanders make informed decisions.

BRANZ Senior Economist Matt Curtis says as we come to the end of 2025, we can clearly see a welcome shift for aspiring homeowners whether they want to build or buy an existing home, and a timely challenge to the idea that the “grass is greener” overseas.

“Housing affordability is the best it’s been in several years in many of our main centres, especially in Wellington. For young Kiwis weighing up a move to Australia to get ahead, it’s worth taking a fresh look at the numbers here at home,” says Curtis.

“Across the Tasman, prices in the major cities are continuing to surge, pushing ownership even further out of reach. In contrast, our data shows conditions in Wellington, Auckland and other urban centres are improving for entry-level buyers. The grass may not be greener after all.”

Curtis acknowledges that not everyone will view these changes positively.

We appreciate this won’t feel like good news for everyone – especially households who bought at or near the peak and are seeing modest gains or even some continued softening,” he says.

“What we’re seeing now is a period of stabilisation - affordability is improving, building activity is lifting, and that’s a stronger foundation for the market than a sharp swing in either direction.”

National picture: strongest affordability boost in years

Nationally, the picture is brightening as lower interest rates and more stable prices flow through into household budgets:

- The average special 1-year mortgage rate has fallen to 4.43% at end of November 2025, down from the mid-to-high 7% range in late 2023, reducing monthly repayments by over 26% for a typical new borrower.

- If households continue repaying at 2023 levels, a standard 30-year mortgage could now be paid off in around 17 and a half years.

- Cotality’s data has New Zealand’s value-to-income ratio at 7.5, the lowest since 2019. Plus, the time needed to save a deposit is at 10 years, down from almost 14 years in 2021.

However, improvements are uneven. Many provincial areas are seeing year-on-year price increases, which support equity for existing owners but limit the affordability gains for first-home buyers. Larger urban centres, particularly Auckland and Wellington, have seen softer price movements, allowing the drop in interest rates to feed more directly into improved serviceability.

Curtis says this mix of conditions is exactly why independent, data-driven tools that incorporate multiple data sets from a broad range of sources are so important.

“The BRANZ Build Insights tool helps us cut through the noise and see what’s really happening region by region. For some New Zealanders, this is a rare chance to get on the ladder in our major centres. For others, it’s a reminder that housing markets are always shifting – and good investment decisions need to be grounded in robust evidence, not just headlines.”

BRANZ has prioritised housing affordability as a critical issue for Aotearoa New Zealand, working with the sector to better understand the drivers of affordability and support practical solutions that deliver quality, resilient and sustainable homes.

Read the article in The Dominion Post on Monday 15 December 2025.